Next Generation Traveler Information System: A Five Year Outlook

CHAPTER 4. ROLES & MODELS REVIEW

Business models for making NGTIS financially viable have changed significantly in recent years. Business models are the activities associated generating value from the collection and provision of traveler information. These activities can be described in the context of a "value chain", which describes how value is added to a product or service as different actors contribute to the end product. This chapter takes a structured look at the value chain, from data collection to data delivery. Public and private sector participants and their current and potential business models and roles will be discussed for each stage in the chain.

Questions considered include:

- What are private sector models and applications for revenue generation? What are the strengths and weakness and their relevance and appropriateness for public agency use?

- What are the roles of state and federal governments in traveler information services in the next five years? Should public agencies be the content provider? Or should public agencies become the data provider and let the private sector provide content?

4.1 ROLES AND VALUE CHAINS

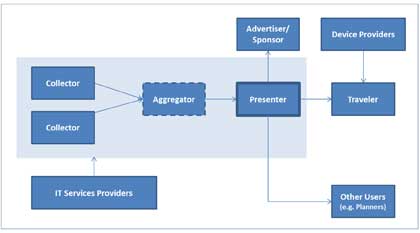

Delivery of traveler information service offerings is a complex business. Public and private sector actors, working both separately and in partnership, bring a variety of agendas and capabilities to the mix. In order to understand the landscape, it is helpful to consider the entire chain of participants and the flow of value, from end-to-end (the "value chain"), as shown in Figure 21.

Figure 21. Chart. Traveler Information Value Chain (SCG)

Roles in the value chain include:

- Collector. Directly captures the traveler information data and generates data products and services.

- Aggregator. Combines multiple data streams and generates data products and services.

- Presenter. Provides the traveler information directly to the consumer. May include everyone from public agencies providing information on roadside DMS and consumer device providers, to mobile app providers and automotive original equipment manufacturers (OEMs) who provide in-vehicle infotainment solutions.

- Device Provider. Provides hardware used by the consumer to interact with traveler information. In some cases, also serves as a Presenter.

- IT Services Provider. Provides services such as software development, hosting, and outsourced operations.

- Advertiser/Sponsor. Links its brand with traveler information in some way to gain business benefit.

- Other Data Users. Specific public and private users of traveler information data, e.g., real estate industry, urban planners, etc.

4.1.1 Role Trends

As traveler information becomes more pervasive, role boundaries are blurring. The private sector has discovered the value of creating consumer crowdsourcing communities. Participating consumers provide much more about themselves and their environment than just traffic data. Instead, traffic is just one piece of the overall consumer Big Data business, an increasingly massive operation with global efficiencies of scale. Traffic is useful in this environment because it is "sticky" – it creates a constant stream of repeat visitors who provide value over time both as a data source and as an ad audience which can be commercialized.

As a result, there is a growing set of 'end to end' providers which handle the entire value chain. These include data mega-managers like Google/Waze. Rather than confining themselves to data collection or a particular aspect of data delivery, they have developed fully integrated solutions complete with cutting-edge end consumer offerings, which have proven very attractive in the marketplace. This places them directly in parallel with similar state activities.

Another major trend is the increasing complexity of the data sourcing picture. The private sector has developed a densely interconnected web of data sharing and aggregating agreements, with more layering on every day. This is partly fueled by the growth of non-infrastructure collection technology options, which has created new categories of participants and expanded the capabilities of existing ones. INRIX and TomTom, for example, have made agreements with auto companies for access to traffic data from their consumer connected car fleets (Marshall, 2014). The potential value of these data have already triggered deals from the OEM side as well, as exemplified by Porsche's recent investment in INRIX. Providers of all stripes are also eyeing the potential of data from the entire national vehicle fleet, which may eventually be mandated for vehicle safety reasons, but can also be used for many other purposes. (Lerman, 2014)

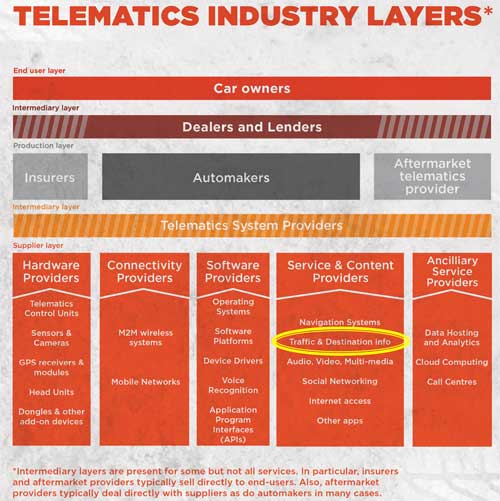

A recent snapshot showing how the data ecosystem around the vehicle has gone well beyond simple traveler information and is now part of the "connected consumer" Big Data pool is shown below in Figure 22 (Lawson, 2015). Traffic is a line item in the overall set of information sent to and received from the car and handled by a wide variety of private sector participants.

Figure 22. Chart. NGTIS / Big Data Landscape Example (Lawson, 2015)

4.1.2 Public Sector Roles

Public sector agencies currently serve in almost every role in the value chain. Given the recent evolution in private sector activities, it is important to assess future public sector roles in NGTIS. The outcome of this assessment will inevitably vary among agencies, so this report seeks to provide some key areas for consideration to assist this process.

4.1.2.1 Collector

Federal law as noted in Safe, Accountable, Flexible, Efficient Transportation Equity Act: A Legacy for Users (SAFETEA-LU) Section 1201 Real-Time System Management Information Program (RTSMIP) requires public sector agencies to provide certain traveler information. The larger question is how much of this requirement the public sector fulfills directly (using its own infrastructure) or indirectly (sourcing the data from other collectors). Numerous public-private partnerships already show that there can be value in a variety of solutions to this question.

Key factors to consider include:

- Pricing. What is the "per unit" cost of information collection? Who can most cost-efficiently capture each type of data? Determining appropriate metrics and tracking them over time will help to resolve this question.

- Compliance risk. Acceptable risk to regulatory compliance if there are contract or supply issues with outsourced vendors.

- Delivery risk. Acceptable risk to ongoing operations if there are contract or supply issues with outsourced vendors. This includes stability of potential vendor companies.

- Switching costs. Are there multiple sources for a given type of data? What will it take to switch from one data source to another?

Presenter

It is important to understand the opportunities and limitations at each point in the value chain. The Presenter has the most access to the consumer and other end users. Those further back in the chain have much more difficulty establishing a consumer brand, and can be more easily replaced by similar offerings. They also do not have direct access to consumer interactions and data.

The public sector has been moving forward along the chain, with the 511 brand and social media push taking it squarely into the Presenter space. This creates direct conflict with the private sector entities who want to own that customer interaction. As private sector data providers move aggressively to capture the traveler's limited attention, the traveler must choose between their offerings and those of the public sector.

Key questions for the public sector to consider include:

- Can agencies achieve their goals without direct customer access? Historically, the public sector has distributed information through channels such as radio and TV. Is that sort of dis-intermediated positioning still acceptable?

- How much of an audience does the direct public sector offering need to reach? Which audience segments are most important?

- How valuable is direct consumer feedback for data collection and customer satisfaction monitoring? "Value" should be measured by metrics here.

- How will the public sector compete over time with consumer-facing brands like INRIX and Google for this role?

4.2 BUSINESS MODELS

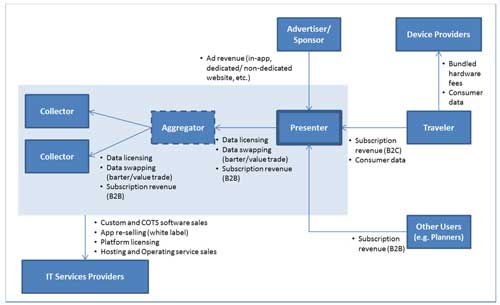

As the private sector continues to the explore opportunities in the traveler information space, corporate whiteboards fill with lists of value creation opportunities like the one shown below in Table 5. Reviewing the marketplace, practically every permutation of these is being tested somewhere. Companies are selling data for license fees, trading consumer's functionality for data, providing data aggregation as a service, etc.

Table 5. Value Creation Opportunities (SCG)

| Where’s the value? |

What’s the deal? |

- Historical databases

- Real-time databases

- Predictive databases

- Apps (development or white label)

- Communications (e.g., radio)

- Development, deployment and operations

- Data collection infrastructure

- Data management system

- Data delivery system (Application Programming Interfaces, Platforms, User Interfaces, etc.)

- Consumer hardware

- Consumer software

- Apps (development or white label) – in-vehicle or mobile

|

- Data licensing

- Data swapping (barter/value trade)

- Ad revenue (in-app, dedicated/non-dedicated website,

etc.)/sponsorship

- Subscription revenue

- Bundled hardware fees

- App re-selling (white label)

- Platform licensing

- Hosting/operating

- Niche markets (real estate)

|

Shown in Figure 23 in the context of the value chain described in the prior section, these value creation opportunities vary by role. It is important to recognize that the private sector reviews both roles and the business models associated with them on a continuous basis, and that every discussion about a business deal takes place with this thinking as a backdrop.

Figure 23. Chart. Value Chain / Value Opportunity Review (SCG)

4.2.1 Public Sector Business Models

The term "business model" typically refers to an approach which generates revenue. Because the public sector is different from a for-profit business, and has significant restrictions on any activities of this type, the role is to create value. In some cases, however, there may be room for some value creation. Several possible areas include:

- Selling or bartering travel data. Limited licensing arrangements, which require fees or 'in-kind' barter, may be possible for commercial use of state data. This approach only works as long as states have data which private sector cannot source less expensively on its own.

- Selling or bartering consumer data. This is a particularly difficult area, as there are major privacy concerns. However, there may be opt-in scenarios in which consumers allow sharing of some information under appropriate circumstances.

- Selling advertisements or sponsorships. Successful ad sales require large volumes of consumer exposure (e.g., traffic on a web page), or a high value niche customer base. To date, states have reported very limited success in establishing sufficiently attractive advertising opportunities (e.g., around 511 websites). This model is very well-established in the private sector, however, and should not be discarded without consideration if local regulations permit it.

- Selling or bartering access to physical assets. Public sector agencies may have access to rights of way and/or infrastructure which can be made available to private sector companies in exchange for data or other related services.

All of these models have major challenges for public sector implementers, and in many cases, regulatory and commercial realities may dictate that the public agency simply internalize the entire value equation without the expectation of external revenue or barter value being added to traditional funding sources. In these cases, business model choices revolve more around the roles taken by the agency (as discussed previously in the section titled "Public Sector Roles") and the opportunity for cost savings due to internal efficiencies and expenditure avoidance.

This last item is particularly interesting in the context of the situation which has evolved in the private sector telematics space. Automakers initially viewed telematics services as a revenue generator, but over time recognized that their primary value was in the internal use of the data captured from vehicles. From a public agency perspective, NGTIS activities may prove to work in a similar way. For example, the user feedback loop created by social media distribution of traveler information may produce valuable insights on how best to influence consumer behaviors, allowing more efficient deployment of resources.

Determining possible business models may be done using a structured process such as the "business model canvas." A detailed case study on exploring value creation opportunities in the public sector using this canvas and related tools may be found in Business Models and Value Creation: A Case Study of the New York City Economic Development Corporation (Chambers & Patrocinio, 2011).