Traffic Incident Management Cost Management and Cost Recovery

Mid-Level Briefing

Photos: iStockphoto

Printable Version [PDF 1.07MB]

You may need the Adobe Reader to view the PDFs on this page.

slide 1

Traffic Incident Management Cost Management and Cost Recovery

Mid-Level Briefing

Photos: iStockphoto

slide notes

Development Notes: This presentation is intended to be delivered to mid-level transportation agency managers to facilitate change towards Cost Management and Cost Recovery for traffic incident management.

slide 2

Agenda

- Briefing Objective and Overview

- Statement of the Problem

- Moving Towards a Sustainable TIM Program

- Action Plan

slide notes

This briefing is intended for mid-level managers who will be responsible for implementing and managing TIM Cost Management and Cost Recovery concepts. Topics covered in this presentation include: Overview and Objectives of the Briefing, Statement of the Problem, characteristics of a sustainable TIM Program, and an action plan for implementation.

slide 3

Overview of Traffic Incident and Event Management

- Effective TIM programs form the basis for preparedness for other transportation emergencies

- All effective programs include close coordination with public safety officials

slide notes

Traffic incident management consists of a planned and coordinated multi-disciplinary process to detect, respond to, and clear traffic incidents so that traffic flow may be restored as safely and quickly as possible. Effective TIM reduces the duration and impacts of traffic incidents and improves the safety of motorists, crash victims and emergency responders. The mission of TIM directly supports the goal towards zero deaths by identifying processes and procedures for all roadway users and specifically the high risk group of emergency responders.

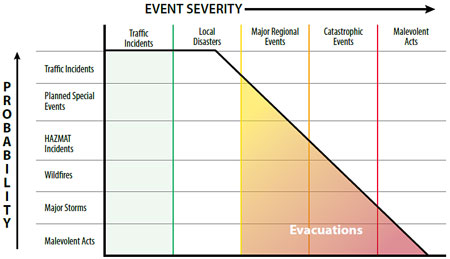

Transportation emergencies can take many different shapes and sizes. The emergency transportation operations continuum shown here indicates that traffic incidents are typically the least severe transportation operations event and are also the most frequently occurring. On this basis, it is understandable how an effective TIM program can help improve overall preparedness for transportation emergencies of all types. This may be true because agency coordination, communication, cooperation and collaboration are some of the most important factors to successful TIM and since many of the stakeholders are constant across the ETO continuum, TIM events can be used to set the foundation for successful large scale event management and mitigation.

slide 4

Overview of Typical Traffic Incident Management Activities

| TIM Strategic Activities | TIM Tactical Activities | TIM Support Activities |

|---|---|---|

|

|

|

slide notes

Activities associated with a TIM program can be classified into three different categories:

- Strategic activities provide the underlying basis for organizing and sustaining a program.

- Tactical activities are completed at the scene of a crash and can also include the policies in place to guide on-scene activities.

- Support activities include tools and technologies that are implemented to improve incident detection, response and clearance.

Each of these activity categories has associated costs that can be managed and may be recoverable. Not surprisingly, tactical activities receive the greatest amount of attention regarding cost recovery. Since that involves physical activities at the scene of crashes, that could be expected. At transportation agencies there are significant costs for equipment needed to respond to scenes; however, that equipment is typically dual use between maintenance activities and TIM activities. In the strategic category, the greatest cost is on resource utilization. This could be expected to be the category least capable of recovering costs but does provide an excellent opportunity for cost management. Support activities can also be a source of significant TIM expenditures, especially to transportation agencies. By developing and implementing systems to achieve interoperability and improved performance measurement, transportation agencies bear great costs.

slide 5

Background

- Current legislation enabling first responders to collect fees is enacted at the local level

- An opportunity to recover costs is with modification to state statues that stipulate recovery of costs for damages to infrastructure

- Tactical TIM costs should be viewed as part of the recovery process, including first responder costs

slide notes

Local municipalities and cities are struggling with the public perception that enacting ordinances to collect fees from drivers who need TIM is over taxation and many localities that have enacted these fees have repealed them or stopped enforcing them. The best opportunity to achieve legislative cost recovery could be through modification to state statutes that allow for cost recovery when infrastructure is damaged. Many of these statutes have been enacted since before the value and need of TIM was recognized. Including tactical TIM costs as recoverable in these statutes could help offset some of the cost.

slide 6

Statement of the Problem

- TIM will continue to be required

- Over 5 million reported crashes in 2009

- Nearly 31k fatalities and over 1.5 million injured

- A minimum response of police, fire/rescue and towing with coordination with transportation

slide notes

According the National Highway Traffic Safety Administration's General Estimate System, the number of Reported Motor Vehicle Crashes in 2009 totaled 5,505,000. While many sources suggest that only half of all motor vehicle crashes are reported, typically only those reported require response and result in the expenditure of responder agency resources. Of these reported crashes, 30,797 resulted in fatalities and 1,517,000 included injuries. Each of these fatal and injury crashes results in a major incident on the roadway that requires a significant level of response—at a minimum police, fire/rescue, and likely towing.

slide 7

Statement of the Problem

- Fiscal impacts of TIM will continue

- Tactical costs can exceed $200k

- There are no tabulations of costs associated with strategic and support activities

- Other costs such as insurance, responder training, lost wages by injured first responders, and other societal costs are unknown

slide notes

If TIM cost management and cost recovery are to become important to an agency, then it is important to understand exactly all costs associated with TIM. There is currently not a consistent understanding of total cost of TIM response and management, particularly costs associated with strategic and supporting elements of a TIM Program.

slide 8

Cost Recovery Defined

- Reimbursement received from outside sources

- Examples: Federal grant sources, MPOs, or private interest

- Cost recovery vs. cost substitution

slide notes

Costs are classified as being recovered when the program receives reimbursement from sources outside of the budget that is then used to fund the program. Cost recovery would involve sources outside the Governor's budget purview, such as costs recovered from Federal grant sources, metropolitan planning organizations, or private interests.

Understanding the difference between cost recovery and cost substitution is a key consideration. Cost substitution is simply replacing a portion of the budget used for incident response from another source within the same budget; for example, moving funds between State agencies.

slide 9

Cost Management Defined

- There are four fundamentals of cost management

- Cost Planning

- Cost Tracking

- Cost Analysis

- Evaluation and Decision

slide notes

Cost management can be broken down into four different fundamental areas: Cost Planning, Cost Tracking, Cost Analysis, and Evaluation and Decision making. Each is interdependent on the other, as this diagram shows.

slide 10

Cost Management Defined

- There are four fundamentals of cost management

- Cost Planning

- Estimating future costs

- Budgeting

- Cost Planning

slide notes

Cost Planning is simply estimating future costs and budgeting. Budgets are based on knowledge about historic costs that has been gained in large part from good tracking and analysis. Budgets for new activities or expansions may include detailed analysis of a capital purchase (e.g., equipment, software).

slide 11

Cost Management Defined

- There are four fundamentals of cost management

- Cost Tracking

- Discrete coding of activities

- Timesheets

- Vehicle mileage

- Supply purposes

- Discrete coding of activities

- Cost tracking represents an opportunity to use NIMS for TIM

- Cost Tracking

slide notes

Cost Tracking involves coding discrete activities and their associated costs or cost drivers, such as personnel time sheets, vehicle mileage logs, supplies purchases, and contract payments.

Often there is a demonstrated need to implement the National Incident Management System with TIM, and the cost tracking fundamental of cost management is where NIMS can affect the financial aspect of TIM.

slide 12

Cost Management Defined

- There are four fundamentals of cost management

- Cost Analysis

- Data processing

- Trends over time

- Per-unit measures

- Output performance measures

- Data processing

- Cost Analysis

slide notes

Cost Analysis requires cost data processing to create cost information—information that will be useful in evaluation, decision-making, and planning. Analysis can produce any of a wide variety of measures across a number of dimensions, including time trends, percentages, and per-unit measures. Examples of static, per unit measures include agency employee hours per incident and labor cost per incident. Examples of temporal analysis measures include trends in labor rates and trends in fuel costs. Examples of percentage measures include labor cost and fuel cost as a percentage of total operating costs.

It is important to recognize the importance of cost analysis to performance measures. Performance measures need to be outcome based, but to arrive at those types of performance measures, outputs must be created. Cost analysis can be used to create the financial connection to performance measures.

slide 13

Cost Management Defined

- There are four fundamentals of cost management

- Evaluation and Decision

- Future programming considerations

- Information for cost planning

- Resource allocations

- Asset management

- Evaluation and Decision

slide notes

Evaluation and Decision. Cost information produced in the analysis stage is evaluated to support decision-making for future programming, resource allocations, and asset management; to support cost recovery mechanisms; and to support appeals to higher level decision-makers for continued or enhanced funding. Subsequent chapters within the Primer address evaluation and decision factors in detail.

slide 14

Cost Management Case Study – South Dakota

- Implemented an ABC system as part of a management performance program known as Collaborative Performance Management

- Helps the department run its operations more efficiently

- Results

- Lower the lifetime cost of ownership and operation of specific assets.

- Allows monitoring of the effectiveness of the department's transportation services.

- Maintains the knowledge base as staff retires.

- Prepares performance-based business plans and budgets.

slide notes

A sound cost analysis approach can be a useful tool for performance management, revealing both ways to achieve a more cost-effective level of performance as well as opportunities to improve performance (e.g., incident clearance time) without increasing cost. Agencies may use a variety of cost analysis approaches, one of which is activity-based costing (ABC). ABC first became popular in the late 1980s in the manufacturing sector, eventually becoming of interest to financial and governmental functions in the 1990s. ABC focuses on discrete processes (activities) and their specific costs and attempts to allocate both direct costs and indirect costs based on carefully determined process cost drivers. That is, ABC defines "cause and effect" relationships to assign costs objectively. The method can be particularly helpful in revealing "true" costs in instances where there is a great deal of indirect cost sharing (e.g., equipment with multiple uses). This example from South Dakota shows how ABC cost management is being applied.

The South Dakota Department of Transportation (SDDOT) implemented an ABC system as one component of a comprehensive management performance program known as "Collaborative Performance Management" (CPM). CPM helps the department run its operations "like a business." The agency credits CPM with significant improvements in performance, including millions of dollars of savings annually. One benefit of the CPM SDDOT is managers have cost and other performance information at their fingertips. They use this business intelligence to reduce the cost of processes, lower the lifetime cost of ownership and operation of specific assets, monitor the effectiveness of the department's transportation services, maintain the knowledge base as senior staff retire, and prepare performance-based business plans and budgets. Says Roxanne Rice, Fiscal and Public Assistance Director of SDDOT, "We are able to show our stakeholders how we are doing, what we are doing, why we are doing it and what it costs the taxpayer."

Source: SAS, Extending the Power of Cost Management in Government White Paper available online at http://www.sas.com/resources/whitepaper/wp_3573.pdf

slide 15

Cost Management Defined

- Costs can be categorized in three ways

- Fixed costs

- Variable costs

- Mixed costs

slide notes

Within the cost tracking fundamental, costs should be classified as either fixed, variable or mixed:

- Fixed costs are costs that typically do not change (in total) in response to changes in volume of activity. Examples include depreciation, supervisory salaries, and maintenance expenses. In reality, such cost elements may change with a change in the scale of the activity, but such changes would not occur in a 1-year analysis period. In microeconomics, a fixed cost (e.g., rent) is one that cannot be varied in the short run.

- Variable costs are costs that change in response to the changes in the volume of activity. We generally assume that the relationship between variable costs and activity is proportional. For example, if the volume of activity increases by 10 percent, then variable costs in total would be expected to rise by 10 percent. The labor cost of employees responding on the scene of an incident would be a variable cost that increases with the number of incidents.

- Mixed (or "semi-variable") costs are costs that contain both a variable cost element and a fixed cost element. An example is a vehicle rental that is billed at a base rate plus a per-mile charge.

slide 16

Moving Toward TIM Program Sustainability

- Implement accounting procedures that allow for a true understanding of all TIM Costs

- Consider activities that allow costs to be recovered

slide notes

Understanding the full cost effect that a TIM program has on an agency and its stakeholders is essential before recovery can be sought. A program that sustains itself will consist of a focus on both the management and recovery of costs.

slide 17

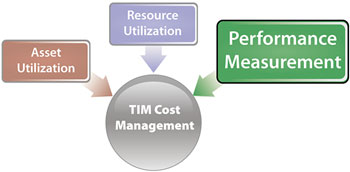

A Roadmap for TIM Cost Management

- Asset Utilization

- Consists of the process to understand costs of devices, facilities and other physical, non-human TIM program elements

slide notes

TIM cost management involves three basic elements: asset utilization, resource utilization and performance measurement. Asset utilization and management and asset performance is becoming an important discussion item among other transportation agency areas of business and that should be extended to the traffic incident management program.

slide 18

Asset Utilization & Management

- Assets are defined as quantifiable physical objects, and resources are defined as people and time.

- A decision-making framework focused on the purchase, construction, maintenance, replacement, and retirement of fixed assets.

slide notes

Assets are defined as quantifiable physical objects, and resources are defined as people and time. The reason for making the distinction for TIM is that TIM assets often fall into the tactical and supporting categories, while TIM resources are present in all TIM categories. Asset management is a decision-making framework focused on the purchase, construction, maintenance, replacement, and retirement of fixed assets. Asset management covers an extended time horizon and draws from economics as well as engineering.

slide 19

Asset Utilization

slide notes

The U.S. DOT Intelligent Transportation Systems Joint Program Office maintains an online knowledgebase of links to summaries that detail the benefits and costs of deploying various types of ITS, including those deployed for incident management. The web page also contains links to summaries of lessons learned and lists ITS deployments by type.

slide 20

A Roadmap for TIM Cost Management

- Resource Utilization

- Consists of the process to understand costs associated with personnel (including both in-house and consultant) situations

slide notes

By basing a program on the national incident management system, a method for collecting resource commitments can be obtained and understood by all those involved. Developing and implementing a cost management electronic system will help increase the visibility of TIM as an area of business. Standard accounting methods such as cost-center accounting can be used to gather and compile these costs in a central system.

slide 21

Resource Utilization

slide notes

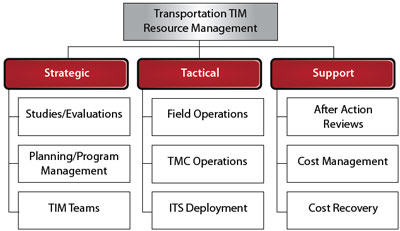

This figure breaks down transportation resource management into the Strategic (Planning and Preparedness), Tactical (Response), and Support (Recovery) Activities categories, with Cost Management and Cost Recovery opportunities housed under the Support category.

Use of the multi-disciplinary approach to TIM resource utilization would create a need to track costs closely, especially with transportation agencies. For this reason, implementing a "cost center" accounting practice is appropriate. This type of accounting can begin to be integrated into transportation agencies for capturing TIM costs from different divisions within the agency. This type of cost accounting will also be applicable as multi-disciplinary TIM resource utilization occurs. A cost center is defined as an area, machine, or person to whom direct and indirect costs are allocated. Each cost center is a distinctly identifiable department, division, or unit of an organization whose managers are responsible for all associated costs and for ensuring adherence to its budgets.

Dividing an organization into cost centers allows several goals to be obtained:

- Assigning costs to cost centers helps determine where costs are incurred within the organization.

- If costs are planned at the cost center level, cost efficiency can be checked at the point where costs are incurred.

slide 22

A Roadmap for TIM Cost Management

- Performance Measurement

- Consists of understanding what benefit assets and resources are providing to the system or what implications that lack of assets and resources are having on overall performance.

slide notes

The importance of performance measurement continues to be more fully understood everyday and that also applies to TIM. A cost analysis process must use TIM performance measures that are tied to economic impacts as a basis to be a valuable tool.

slide 23

Performance Measurement

- FHWA has been researching and developing information on TIM performance measures

- A knowledge base has been developed or use by practitioners

- https://ops.fhwa.dot.gov/tim/preparedness/tim/knowledgebase/

slide notes

While not strictly "cost management," developing performance measures and making comparisons to TIM costs provide useful information to TIM managers and, perhaps more importantly, help to "sell" TIM to the public and those making funding allocation decisions. Like most efforts that transportation agencies engage in, TIM must be able to show what benefit is being realized when compared to the cost being incurred. Performance measurement is a key component to being able to demonstrate the benefit of money spent. The combination of understanding the costs of TIM through cost management that is linked to the performance result will ultimately become one of the key factors of cost-benefit analysis.

slide 24

A Roadmap for TIM Cost Management

| Category | Start-up Plan | Transition Plan | Established Program |

|---|---|---|---|

| Asset Utilization |

|

|

|

| Resource Utilization |

|

|

|

| Performance Measurement |

|

|

|

slide notes

Many agencies are not yet ready to execute a TIM cost management process. This roadmap provides direction for starting a TIM cost management process where none currently exist, and then transitioning the start-up program into an established aspect of the TIM program.

slide 25

Options for Recovering Costs

- Seek and support legislative actions that enable recovery

- Examine opportunities for public-private partnerships

Photo: iStockphoto

slide notes

Once TIM costs are fully understood, additional cost recovery methods may be revealed. At this point in time there are two strategies to pursue to enable transportation agencies and all TIM stakeholders to conduct cost recovery activities. The ability to collect fees from road users that require response typically require legislation. Existing legislation is currently at the local level through individual ordinances. Public-private partnerships will continue to be examined as a way for transportation agencies to reduce their spending and that also applies to traffic incident management.

slide 26

Types of Legislation

- Emergency Medical Services – costs associated with response and patient transport.

- Fire – costs associated with response and recovery activities. Actions essential to the survival of the vehicle occupants, such as extrication.

- HAZMAT – costs associated with the emergency response and recovery efforts due to the release of hazardous materials from responsible parties.

slide notes

Each TIM stakeholder has different ways that they attempt to recover costs. As can be seen, the desire or necessity to recover costs associated with TIM is not a new activity.

slide 27

Types of Legislation

- Infrastructure – costs associated with the repair or replacement of the roadway or roadway components from liable drivers.

- Law Enforcement – costs associated with response and/or crash investigation from involved parties or insurance companies.

- Transportation – costs associated with response and traffic control.

slide notes

Additional methods used to recover costs for specific activities and agencies. Again, the desire or necessity to recover costs associated with TIM is not a new concept.

slide 28

Legislation Awareness

- It is important to use caution when discussing cost recovery legislation.

| Proponent Viewpoints | Opponent Viewpoints |

|---|---|

|

|

slide notes

When participating in discussions regarding TIM cost recovery it is important to understand the issues. A lot of information has been created and disseminated by proponents and opponents. This diagram shows some of the core points used by both groups.

slide 29

Public-Private Partnerships

- Many transportation agencies already use these partnerships with safety service patrol programs

- Expand TIM cost considerations and seek these types of partnerships:

- The sale of traffic data to private vendors

- Implementation of HOT lanes and the inclusion of TIM costs as a part of the calculated costs

slide notes

Many foreign countries such as Australia and New Zealand have privatized transportation operations, including TIM. In New Zealand for example, the Transport Agency awards long-term road network management contracts where the contractor acts on behalf of the agency. This is similar to the intelligent transportation system delivery and procurement methods used in some states where a systems manager is hired. This by itself though, is not cost recovery. The next step for many of these countries is to allow the network manager to introduce concessions for services. Until that can be examined more fully for applicability for the US, TIM cost calculations should be considered when determining rates for selling traffic data and implementing high occupancy toll lanes.

slide 30

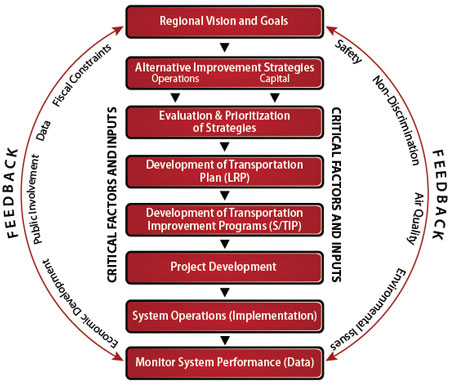

Planning for TIM

- Include the outcome of a formalized TIM program into a planning for operations strategy

- Alternative Improvement Strategies

- Evaluation and Prioritization of Strategies

- Development of Transportation Plans

- Project development process

- Systems operations

- System Performance

slide notes

FHWA is currently developing guidance on how to link TIM to the planning process. The transportation planning process is most effective through collaboration among an appropriate range of stakeholders. TIM managers need to be part of the collaborative process. Planners may often be able to supply data about where current or future mobility issues will arise, and TIM managers can provide input on the operations objectives and strategies they believe would be most effective to implement. The following points in the transportation planning process could benefit from the involvement of TIM managers.

- Alternative Improvement Strategies – Provide TIM Strategies – TIM managers have the opportunity to suggest operational solutions for the investment decisions that support the objectives. TIM managers can best give input on the operations strategies that can be most effective in particular situations.

- Evaluation & Prioritization of Strategies – Provide TIM Cost Data and Performance Index Information – TIM managers can provide data that yields a better understanding of the effectiveness of operational strategies and the advantages in relation to or in complement to other strategies.

- Development of the Statewide/Metropolitan Transportation Plan – Provide Support for Consideration of TIM – TIM managers can provide supporting information during the process for inclusion of policies, goals, objectives, and strategies that facilitate TIM. Resulting MTPs should be the proper mix of capital and operational projects to optimize system performance within the fiscally constrained plan.

- Project Development – Provide TIM Project Detail – TIM managers can provide detailed information necessary for project development.

- Systems Operations – Operate the System – TIM managers can operate their program.

- Monitor System Performance – Track Performance Measures - Performance measurements are a key means of assessing the effectiveness of the strategies. TIM managers need to provide input to system performance.

slide 31

Planning for TIM

- Connecting TIM with State and Regional Transportation Improvement Plans

- Congestion Mitigation and Air Quality

- National Highway System

- Surface Transportation Program

slide notes

TIM operational costs or related capital costs may be included in the TIP as a line item or specific project. Their inclusion is based on funding eligibility and available funding. Funding is generally provided at an 80 percent Federal share with a 20 percent local match. The following Federal-aid categories include eligibility for TIM related costs:

Congestion Mitigation and Air Quality (CMAQ)

Purpose: Provides funding for projects and programs in air quality nonattainment and maintenance areas for ozone, carbon monoxide, and particulate matter, which reduce transportation-related emissions.

Specific Eligibility: traffic management/monitoring/congestion relief strategies.

National Highway System (NHS)

Purpose: Provides funding for improvements to rural and urban roads that are part of the NHS.

Specific Eligibility: capital and operating costs for traffic monitoring, management, and control facilities and programs.

Surface Transportation Program (STP)

Purpose: Provides flexible funding that may be used by States and localities for projects on any Federal-aid highway.

Specific Eligibility: capital and operating costs for traffic monitoring, management, and control facilities and programs.

The competition for available funding in the S/TIP makes decisions on project inclusion extremely difficult. This reinforces the need for TIM manager involvement in the transportation planning process, for a solid for cost management process, and for using performance measures for TIM.

slide 32

Planning for TIM

- Creating Local Line Items

- Helps anticipate costs

- Helps administration, politicians and public account for and acknowledge TIM

- Helps with performance measurement

slide notes

Regardless of a local jurisdiction's cost recovery process, including a line item in an agency or city/county budget can be helpful as a cost management tool. A TIM line item is an excellent way for administrators, politicians, and the general public to account for and acknowledge the cost of TIM services so they can be measured against the benefits they bring to the community. It can also motivate those involved in the tracking process to accurately account for appropriate costs. This can facilitate decision making by State and local leaders.

The use of a budgetary line item is not only a sound cost management tool, it is also imperative for justifying additional resources for TIM programs.

slide 33

Action Plan

- Support and Execute TIM programs that have strategic direction and multi-disciplinary participation

- Implement the Cost Management Roadmap

- Coordinate with DOT executives and industry points of contact to identify and vet cost recovery methods

slide notes

The action plan for moving towards a sustainable TIM program includes three core activities. First, executing a TIM program that includes a strategic direction is essential for predicting costs and right-sizing the program. Using the cost management roadmap as a guide will help organize costs in a manner that is appropriate as recover is considered. Finally, developing the ability to recover TIM costs with DOT Executives and private industry points of contact will help identify ways to further streamline services and ultimately, reveal additional ways to recover costs.