Priced Managed Lane GuideCHAPTER 5. Finance and Procurement5.1 Funding and Financing Priced Managed Lane ProjectsIn many respects, paying for the cost of a priced managed lane project is not unlike paying for any other transportation improvement project. A wide range of federal, state, and local funding sources and financing tools can be used to pay for priced managed lane improvement. Projects may use a combination of federal-aid program and state match funding like most transportation improvements, or rely partially or substantially on toll-backed debt financing. In addition, private equity and additional financing options available to private sector participants can be used for projects implemented on a P3 basis. The one characteristic distinguishing priced managed lane projects from typical highway improvement projects is that they generate toll revenue. However, as shown earlier in Table 2-1, the amount of revenue can vary significantly. The amount of revenue priced managed lane projects generate determines the degree to which projects can pay for themselves, support a debt-financed package, cover ongoing operational and maintenance costs, or generate excess revenue for reinvestment by the project sponsor or retention by a private development partner. 5.1.1 Project ScaleIt is helpful to characterize priced managed lane projects as Small, Medium, or Large, based on project scale and cost. Where a project falls along the scale/cost spectrum can help inform project funding and financing considerations. Table 5-1 presents general project and financial characteristics of Small, Medium, and Large priced managed lane projects. The scale of priced managed lane projects is driven largely by whether they involve the conversion of existing highway capacity to tolled operation or the expansion of existing corridors. The capacity for revenue generation is driven by the scope of the projects, congestion in the corridor, and the willingness of motorists to pay to avoid it. Projects with two or more priced lanes per direction are more likely to generate significant cash flows. The capacity for revenue generation has a substantial influence on the extent to which projects can be debt financed and whether they might attract private sector interest. In this case, projects would need to generate sufficient revenue to cover ongoing operations and major maintenance costs, and generate excess revenue available for return on a private sector equity position. Conversely, some smaller projects may require ongoing subsidies to pay for operations and maintenance. 5.1.2 Lifecycle Project CostsCapital Costs. Capital costs include all implementation costs related to the design and construction of the project, including right-of-way acquisition and utilities relocation. For priced managed lane projects, this cost can vary from several million dollars to over $2 billion, depending on the scale of the project as presented in Table 5-1. A simple HOV-to-HOT conversion, like the $18 million SR 167 HOT Lanes may involve only the purchase and installation of electronic toll collection equipment, other related ITS infrastructure, signage, and restriping the existing HOV lane to provide six northbound access zones and four southbound access zones. The $1.3 billion I-15 Express Lanes incurred significant capital costs from the construction of two to four additional travel lanes, direct-access ramps to park-and-ride lots, overpass reconstruction, and a moveable barrier that allows HOT lane reconfiguration in the predominant direction of travel, along with ETC and ITS equipment and signage. Financing Costs. Financing costs are relevant to projects that use finance tools to help pay for a project’s capital costs. These are the associated fees paid to financial advisors, rating agencies, banks, lawyers, and other institutions involved in evaluating, arranging, or issuing individual or packaged debt and credit instruments. In addition, the interest paid on any loan made to the project is a financing cost. Typically financing costs are considered together with capital costs in defining a total project cost during implementation. These costs can be substantial but potentially worth the price of alternatively delaying project implementation or not implementing the project at all. As one example, the financing costs for the 495 Express Lanes represent about 25 percent of the total $2.1 billion project cost (capital plus financing). Operations and Maintenance (O&M) Costs. O&M costs are a key consideration to a priced managed lane project because the success of the facility depends greatly on continuous, high-quality operation that involves managing user access and determining and collecting the appropriate toll. In addition, there is often an expectation of a higher level of customer service with priced managed lane facilities, including lane availability, condition, and incident response. Major maintenance costs can be significant considerations as well, since the upgrade or replacement of toll collection equipment as technology advances may be necessary over a mid- or long-term operational period. O&M costs need to be estimated and programmed carefully and a determination made whether toll revenue can and will be used to pay for these costs or if supplemental resources will be necessary. Forecasted usage, toll increase (or decrease) policies, and vehicular exemptions need to be taken into account. Conceivably, a budget independent of toll revenue may also be established to pay for O&M. 5.2 Revenue Sources5.2.1 Traditional Federal and State FundingTraditional federal and state funding includes federal and state motor fuel taxes and other state motor vehicle fees and taxes, such as vehicle registration and driver’s license fees. Funding allocations for these monies generally follow a formulaic process prescribed at the state level that takes into account population, roadway mileage, and need-based metrics. In urban areas of 50,000 or more people, MPOs manage decisions about which projects to fund, based on their transportation planning and programming process. Elsewhere, state departments of transportation manage these decisions. Priced managed lane projects may receive funding from these traditional sources in the same manner as any other improvement project considered in transportation planning and financial programming processes. Further information on these processes is available at http://www.planning.dot.gov/documents/BriefingBook/BBook.htm. 5.2.2 Discretionary GrantsHistorically, many priced managed lane projects relied in part on federal grants through the Value Pricing Pilot Program, but with the expansion of tolling authority under MAP-21 (see Section 3.4.1) and no additional funds authorized after Fiscal Year 2012, the program is not expected to be a significant source of future funding. Several recently implemented projects also received funding as part of the one-time Urban Partnership Agreement (UPA) and Congestion Reduction Demonstration (CRD) programs initiated in late 2006 and late 2007, respectively. The UPA and CRD programs were one-time programs funded by USDOT using miscellaneous discretionary grant funds authorized by Congress, rather than programs specifically funded through periodic federal transportation authorization legislation. The programs have provided funding to priced managed lane projects in Atlanta, Los Angeles, Miami, and Minneapolis. Further information is available at http://www.upa.dot.gov/index.htm. The American Reinvestment and Recovery Act of 2009 introduced the Transportation Investment Generating Economic Recovery, or TIGER Discretionary Grant program. The discretionary TIGER grant program awards funds on a competitive basis for projects that will have a significant impact on the Nation, a metropolitan area, or region. TIGER awards have supported priced managed lane projects in Denver (U.S. 36 Managed Lanes), Virginia (I-95 HOT Lanes), and Riverside County, California (SR 91 Express Lanes extension) by providing funding to leverage a potential federal Transportation Finance and Innovation Act (TIFIA) loan (see Section 5.3.2). Additional information on TIGER grants is available at http://www.dot.gov/tiger/. 5.2.3 TollsA natural source of funding for priced managed lanes are the tolls charged for access to the facility. Clearly, toll revenue does not accrue until the facility is operational, and for this reason, is often devoted to ongoing facility operations and maintenance costs. In the case of a network of tolled facilities or managed lanes, toll revenue from existing facilities can be pooled and used to fund a new priced managed lane project on an upfront basis. Facilities with an appropriate level of revenue generation can use tolls in a debt financing capacity to support the issuance of bonds or other credit extended to the project. Bonds and other debt instruments are then paid back over time from future toll proceeds. 5.2.4 Other Revenue SourcesOther revenue sources beyond traditional sources, grant programs, and tolls come from the state and local levels. One of the most noteworthy is state or local sales tax measures. A sales tax measure, often approved by voters, is typically dedicated to transportation purposes and frequently to a specified program of projects. Local sales taxes are popular in California where they are levied at the county level, upon approval by two-thirds of voters, for a prescribed length of time and a prescribed set of projects. The I-15 Express Lanes, I-680 Express Lanes, I-580 Express Lanes, and SR 237 Express Lanes are all beneficiaries of local option sales tax measures. Value capture revenues are another potential source of funds generated at the local level, although to date, they have not been used to fund priced managed lane projects. Value capture mechanisms capitalize on increased land value attributed to specific transportation improvements that enhance accessibility to desirable destinations such as jobs and schools. The revenue generated can help finance the transportation improvement, or it can go toward further transportation investment, spurring a new round of increased accessibility and land value. Among the options for value capture are:

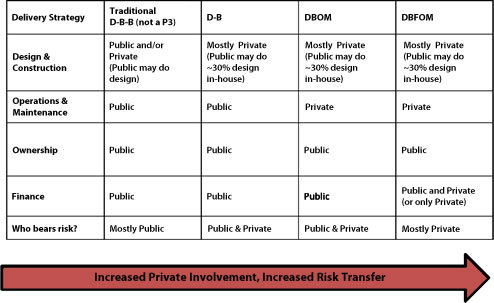

For additional information on state revenue sources, see: https://www.fhwa.dot.gov/ipd/revenue/non_pricing/sources_tools/state.htm. For additional information on local revenue sources, see: https://www.fhwa.dot.gov/ipd/revenue/non_pricing/sources_tools/local.htm. 5.3 Financing Tools5.3.1 Leveraging RevenuesAs noted earlier, priced managed lane projects have the ability to leverage expected toll revenues to help finance a portion or all of a project’s implementation costs. Project finance is typically used with large capital projects where using a “pay-as-you-go” approach is not a viable option. Not all priced managed lane projects generate sufficient revenue to support the issuance of toll-backed debt, however. Revenues from those categorized as Small would generally be considered insufficient, those categorized as Medium may have the potential for some toll-backed debt, and those categorized as Large may be expected to generate sufficient revenue to attract private sector investment. Private sector project financing often includes one or more forms of debt issuance, as well as an equity contribution expected to be recouped over time from the facility’s toll proceeds. It should be emphasized that financing tools do not replace revenue and can only be used when there is a viable revenue source (tolls in the case of priced managed lanes) to make debt-service payments or provide returns on equity. An investment-grade traffic and revenue study is necessary for the issuance of debt backed by the project’s toll revenues. 5.3.2 Federal Credit AssistanceSeveral forms of federal credit assistance are available to project sponsors of priced managed lanes including TIFIA, state infrastructure banks (SIBs), and Section 129 loans. Transportation Infrastructure Finance and Innovation Act (TIFIA). Federal credit assistance is available to priced managed lane project sponsors through the TIFIA program, which provides federal direct loans, loan guarantees, and standby lines of credit to finance surface transportation projects of national and regional significance. The TIFIA program is designed to fill market gaps and by providing improved access to capital markets, flexible repayment terms, and interest rates that are often more favorable than those found in private capital markets. TIFIA can help advance projects that otherwise might be delayed or deferred because of size, complexity, or uncertainty over the timing of revenues. The information that follows reflects the process and requirements of the TIFIA program as implemented by MAP-21. In order to quality for support from the TIFIA program, projects must have a capital cost of at least the lesser of $50 million ($25 million in the case of a rural project) or 33.3 percent of a state’s federal highway assistance for its most recently complete fiscal year. In the case of ITS improvements, the minimum is $15 million. TIFIA credit assistance is limited to a maximum of 49 percent of the total eligible project costs. Projects must have environmental clearance prior to funding obligation and senior debt must be rated investment grade. All TIFIA projects must be supported in whole or in part from user charges or other dedicated non-federal dedicated revenue sources. The exact terms for each loan are negotiated between the USDOT and the borrower, based on the project economics, the cost and revenue profile of the project, and any other relevant factors. Applications are accepted on a rolling basis under which eligible projects must receive assistance, provided adequate funds are available to cover the associated subsidy cost. It is also possible to enter into a master credit agreement, which is an early contingent commitment of TIFIA credit assistance for single projects or a program of projects secured by a common security pledge. The master credit agreement locks in the contingent commitment so long as financial close occurs within three years. Several priced managed lane projects have used TIFIA to date including the 495 Express Lanes in Northern Virginia (see the Appendix of priced managed lane profiles), the North Tarrant Express near Fort Worth, Texas (see https://www.fhwa.dot.gov/ipd/project_profiles/tx_north_tarrant.htm), and the LBJ Express near Dallas, Texas (see https://www.fhwa.dot.gov/ipd/project_profiles/tx_lbj635.htm). Each of these projects has used TIFIA in combination with private activity bonds and private equity, which are discussed in sections that follow. Additional information is available at the USDOT’s TIFIA website: https://www.fhwa.dot.gov/ipd/tifia/index.htm. State Infrastructure Banks. State Infrastructure Banks are revolving infrastructure investment funds for surface transportation that are established and administered by states. A SIB, much like a private bank, can offer a range of loans and credit assistance enhancement products to public and private sponsors of highway construction projects. SIBs are capitalized with federal-aid surface transportation funds and matching State funds. (Several states have established SIBs or separate SIB accounts capitalized solely with state funds.) As loans or other credit assistance forms are repaid to the SIB, its initial capital is replenished and can be used to support a new cycle of projects. All repayments are considered to be federal funds and the requirements of Title 23 of the United States Code apply to SIB repayments from federal and non-federal sources alike. SIBs give states the capacity to make more efficient use of its transportation funds and significantly leverage federal resources by attracting non-federal public and private investment. Alternatively, SIB capital can be used as collateral to borrow in the bond market or to establish a guaranteed reserve fund. Loan demand, timing of needs, and debt financing considerations are factors to be weighed by states in evaluating a leveraged SIB approach. To date, no priced managed lane project has received credit assistance from a SIB. Additional information on SIBs is available at https://www.fhwa.dot.gov/ipd/finance/tools_programs/federal_credit_assistance/sibs/. Section 129 Loans. Section 129 of Title 23 allows federal participation in a state loan to support projects with dedicated revenue stream including tolls, excise taxes, sales taxes, real property taxes, motor vehicle taxes, incremental property taxes, or other beneficiary fees. Similar to state infrastructure banks, Section 129 loans allow states to leverage additional transportation resources and recycle assistance to other eligible projects. States have the flexibility to negotiate interest rates and other terms of Section 129 loans. When a loan is repaid, the state is required to use the funds for a Title 23 eligible project or credit enhancement activities, such as the purchase of insurance or a capital reserve to improve credit market access or lower interest rate costs for a Title 23 eligible project. One important distinction between SIB and Section 129 loans is that projects that receive assistance from repaid Section 129 loans are not required to meet the same number of federal requirements as those using SIB loans. To date, no priced managed lane project has used a Section 129 loan. Additional information is available at https://www.fhwa.dot.gov/ipd/finance/tools_programs/federal_credit_assistance/section_129/. 5.3.3 Bonding and Debt InstrumentsSeveral bonding and debt instrument options are available to priced managed lane project sponsors. These include municipal debt in the form of revenue bonds and Grant Anticipation Revenue Vehicle (GARVEE) bonds backed by future federal-aid funds, as well as private activity bonds and commercial bank loans in the case where a private sector partner is responsible for arranging project financing. Revenue Bonds. Bonding is the primary financial tool available to state and local governments to raise financing covering the cost of public works projects of all types. State and local governments are able to issue debt using the municipal bond market where the interest income earned by the holders of these bonds is exempt from federal tax, as well as state and local taxes if the bonds are issued in the investor’s state of residence. As a result of the tax-exempt status of the income investors receive from municipal bonds, investors are usually willing to accept lower interest rate payments compared to other types of borrowing with comparable risk. This makes municipal debt particularly attractive to state and local governments, as the interest rates are lower than other debt options. In the case of priced managed lane projects, municipal bonds can take the form of revenue bonds backed by future toll proceeds, which are used to make interest and principal payments to the bondholders. GARVEE Bonds. GARVEEs are a form of debt repayable with future proceeds from federal-aid highway funds received by states under Section 122 of Title 23 of the U.S. Code. GARVEE bonds require state enabling legislation, which can be project specific or enable the use of GARVEEs to finance projects on a programmatic basis. GARVEE bonds are a state obligation even though they leverage federal-aid funding. GARVEE bonds may be used to cover the entire cost of projects or larger improvement programs; they are also often combined with other debt and funding mechanisms for larger projects. Further information on GARVEE bonds is available at https://www.fhwa.dot.gov/ipd/finance/tools_programs/federal_debt_financing/garvees/index.htm. Private Activity Bonds. Private Activity Bonds (PABs) are debt instruments issued by State or local governments whose proceeds are used to construct projects with significant private involvement. PABs have long provided a low-cost financing option for various types of public-benefit infrastructure projects, such as ports and water and sewer projects. However, transportation infrastructure had not been eligible for Private Activity Bond financing until the passage of SAFETEA-LU, which added highway and freight transfer facilities to the types of privately developed and operated projects for which PABs may be issued. SAFETEA-LU placed a national volume cap of $15 billion for these facilities, which was unchanged by MAP-21. Private activity is permitted on highway improvement projects while maintaining the tax-exempt status of the bonds. In this manner, private participation in transportation infrastructure is encouraged because borrowing costs are reduced relative to standard commercial debt. In addition, PABs have been an attractive source of capital in a tight credit market where the issuance of commercial debt has been curtailed. The three priced managed lane project examples that have used TIFIA credit assistance have done so in combination with PABs: the 495 Express Lanes in Northern Virginia (see the Appendix of priced managed lane profiles), the North Tarrant Express near Fort Worth, Texas (see https://www.fhwa.dot.gov/ipd/project_profiles/tx_north_tarrant.htm), and the LBJ Express near Dallas, Texas (see https://www.fhwa.dot.gov/ipd/project_profiles/tx_lbj635.htm). Additional information on PABs is available at https://www.fhwa.dot.gov/ipd/finance/tools_programs/federal_debt_financing/private_activity_bonds/index.htm. Commercial Bank Loans. Private sponsors of priced managed lane projects may borrow money from a commercial bank or more likely a syndicate of commercial banks. Borrowing costs to private sponsors, however, are typically greater than to public sponsors, and especially in a tight credit market, PABs have been a more attractive source of debt. To date, no priced managed lane projects have used commercial bank loans as a part of a financing package. 5.3.4 Availability PaymentsAvailability payments are made to a private concessionaire by a public project sponsor based on project milestones or facility performance standards in exchange for particular services. They can be used to compensate the private partner for the design, construction, operation, and maintenance of a priced managed lane facility and can be subject to reduction in the event of not meeting a stipulated performance target. federal-aid grants may be used to pay the capital portion of availability payment installments. Availability payments may be an attractive option to priced managed lane project sponsors who would like to capitalize on private sector expertise in the delivery and operation of the facility but wish to retain control over toll rates and collection. Availability payments are also used when toll revenue itself may be insufficient to cover the full cost of construction and operation. This situation may arise on a project with high costs and low revenue potential or with a priced managed lane project that seeks to balance the potentially divergent goals of maximum revenue generation and maximum utilization. More information on availability payments is available at the American Association of State Highway and Transportation Officials (AASHTO) Center for Excellence in Project Finance: http://www.transportation-finance.org/funding_financing/financing/other_finance_mechanisms/availability_payments.aspx. The 595Express in Fort Lauderdale, Florida is being implemented under an availability payment contract (see the Priced Managed Lane Profiles Appendix). 5.4 Procurement OptionsThe range of procurement options available to priced managed lane projects is the same as for any transportation improvement project, from traditional DBB to those involving greater private involvement, including DB, design-build-operate-maintain (DBOM), and DBFOM. The applicability of an option with greater private involvement depends on certain project characteristics and, more generally, its scale. Small projects would likely only be delivered via traditional DBB. Medium projects may benefit from a DB or DBOM strategy. Large projects may be additionally suited to DBFOM procurements. Other non-traditional procurement options exist, but only the most common are reviewed here. More comprehensive information is available at FHWA’s P3 website. [7] In addition to the procurement strategy descriptions that follow, Figure 5-1 summarizes which party (public or private) is responsible for certain project delivery components for each strategy. Figure 5-2 summarizes risk allocation associated with project delivery components for each strategy. Figure 5-1: Delivery Models and Responsibilities

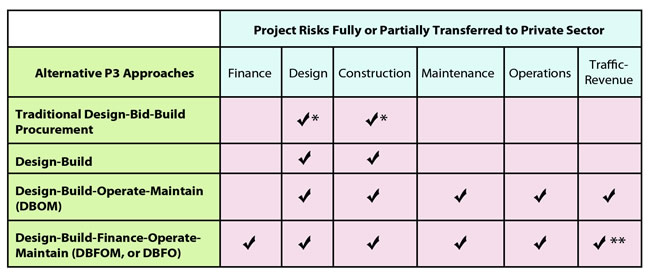

Figure 5-2: Delivery Models and Risk Allocations

* Limited risk transfer ** Traffic revenue risk retained by public sector in availability payment concession 5.4.1 Design-Bid-BuildDesign-bid-Build is the traditional project delivery method where DOTs enter into separate contracts to design improvements and then construct them. The design contract will define the project to 100 percent completion and prepare detailed construction documents. A construction contract then follows, where prequalified contractors are invited to submit bids to construct the project, with the award going to that contractor providing the lowest price. Given that design and construction activities are undertaken by separate entities, it does not incentivize them to coordinate the two activities and seek out design refinements that could reduce construction costs or accelerate construction. 5.4.2 Design-BuildDesign-build is a project delivery method that combines separate services into a single contract. With design-build procurements, project sponsors execute a single, fixed-fee contract for both engineering services and construction with a private sector design-builder. Bidders submit fixed-price proposals and the ultimate contract award is made on a best value approach taking into account cost together with the qualifications of the bidders and the relative merit of their proposals. Given that the award of design-build contracts is driven by cost, design-builders seek to develop cost effective designs that are well suited to their construction techniques. They also look for opportunities to accelerate the completion of the project by overlapping design and construction activities and optimizing the sequencing of construction activities. The fixed-price contract structure is an effective means to transfer cost overrun risks to the private sector. Many design-build contracts also specify completion dates along with penalties in the event that these deadlines are not met, thereby transferring completion risk to the private sector. 5.4.3 Design-Build-Operate MaintainThe DBOM model is an integrated partnership that combines the design and construction responsibilities of design-build procurements with operations and maintenance. These project components are procured from the private sector in a single contract with financing secured by the public sector. This process transfers design, construction, operations, and maintenance risk to the private sector. However, the degree to which operations and maintenance risk is transferred is driven by the length of the operations period. With longer operations periods, this risk transfer may incentivize the private designer-builder-operator to make upfront capital investments to avoid more costly repairs at a later time. It also reduces the risk that issues could go unnoticed or unattended and then deteriorate into much more costly situations. 5.4.4 Design-Build-Finance-Operate-MaintainWith the DBFOM approach, responsibilities for designing, building, financing, and operating are bundled together and transferred to a private sector developer. There is a great deal of variety in DBFOM arrangements in the United States, and especially the degree to which financial responsibilities are actually transferred to the private sector. One commonality with all DBFOM projects is that they are either partly or wholly financed by debt leveraging revenue streams dedicated to the project. Tolls are the most common revenue source. However, availability payments may also be used funded through taxes and/or tolls. Future revenues are leveraged to issue bonds or other debt that provide funds for capital and project development costs. They are also often supplemented by public sector grants in the form of money or contributions in kind, such as right-of-way. While public agencies sponsoring DBFOM projects retain full ownership and ultimate control, DBFOM procurements transfer the maximum risk to the private sector. They are long-term arrangements commonly lasting 30 to 50 years or more. Footnotes [7] https://www.fhwa.dot.gov/ipd/p3/index.htm Back to reference 7. |

|

United States Department of Transportation - Federal Highway Administration |

||